Go Back

Is Atlassian really overvalued?

Atlassian clearly shows signs of overvaluation, but there is more to it

Jira sucks.

Atlassian’s key digital product, used by thousands of developers, designers & managers worldwide is constantly mocked (try googling “Jira sucks”). And it seems that even Atlassian, the company behind the leading development management software agrees: its R&D investment has not decreased since 2020.

Are they going to catch up with competitors like Productboard with their newly released copycat ‘Jira Product Discovery’?

Let’s see. In the meantime, investors seem to have high hopes for Atlassian since its market cap remains way over its intrinsic valuation.

How do we know this?

Atlassian is overvalued… But its growth makes it an interesting bet

Atlassian's current price is above even our highest estimate. To justify it, they'd need a 47% profit margin, despite their best ever being… -4%. So yeah, a bit of a stretch. To put this in perspective, companies like Meta make a 40% net margin.

But the hype will probably last for a while, have a look why below.

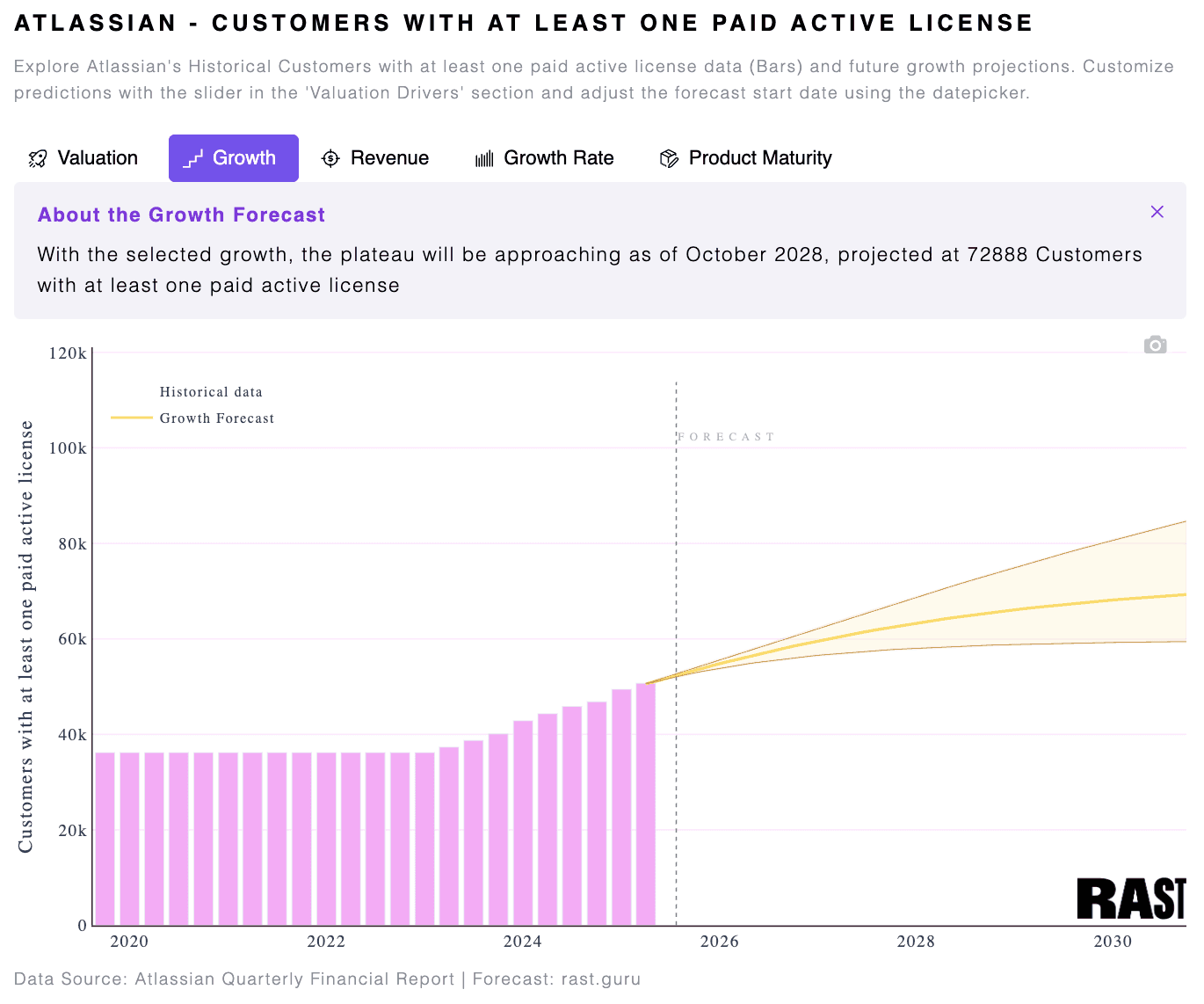

Atlassian's customers are growing nicely

Atlassian's plateau of Customers with at least one paid active license could be reached in October 2028 with 72K users. In the best case scenario, the growth can even further continue.

So yeah, the hype surrounding Atlassian's valuation is real but may continue for a while.

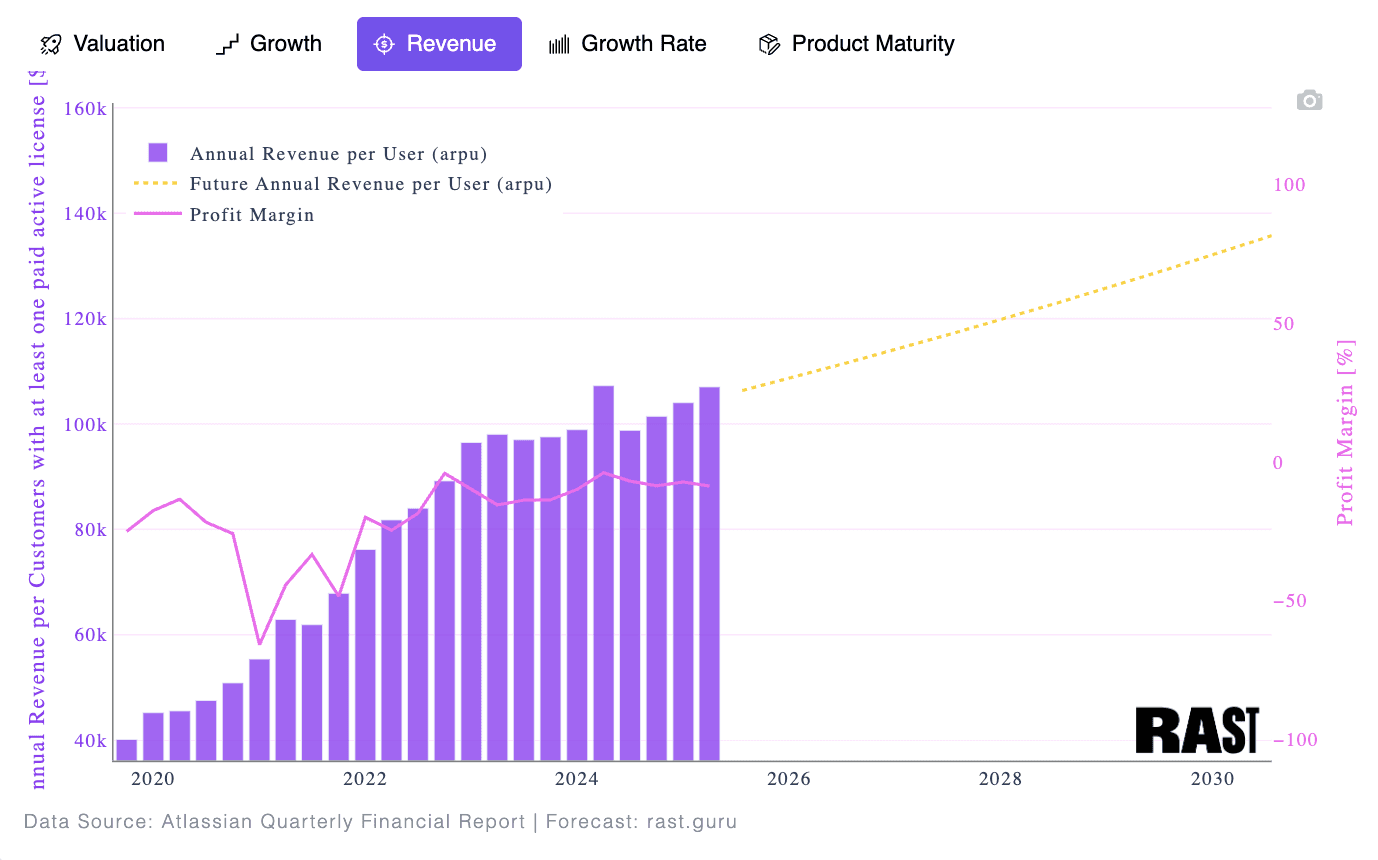

Revenue per customer is still growing

Atlassian's revenue per customer's growth has slowed down since 2022. But it remains strong and steady, with customers being more and more locked in Atlassian's ecosystem.

The product is still massively improving

Atlassian still heavily invests in its product, with over 50% of its revenue reinvested in R&D. This could hint at a sustained growth and an improved revenue per user.

More posts you may like

Jan 26, 2026

·