Go Back

AI's triggered a SaaS sell-off. But it's just a trigger

AI didn't cause the on-going SaaS stock crash, it just lit the fuse on a powder keg that was always there. Most of these companies were simply overvalued.

Open any finance newsletter this week and you’ll read a variation of the same headline: “AI is killing SaaS.” Scott Galloway summed it up nicely:

The sell-off was triggered by a wave of new AI tools that spooked investors. Anthropic rolled out industry-specific products for legal, finance, and customer service. OpenAI launched a more powerful, multi-agent version of its coding tool and a new platform to help companies deploy AI agents.

To top it off, OpenClaw, a new, open-source AI assistant, exploded on social media. Self-dubbed “the AI that actually does things,” it can execute tasks on its own and remember past interactions, allowing it to learn user preferences and perform personalized actions. […]

The sell-off reflects growing concern that AI agents could disintermediate the entire software-as-a-service industry. If companies can build their own software with AI, why would they keep paying for traditional SaaS products?

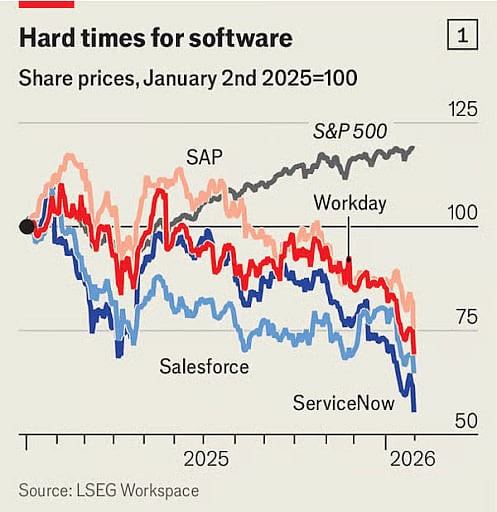

The result? Software stocks plunged while the S&P500 continued to grow.

Software prices plunged compared to the S&P500, https://www.economist.com/business/2026/02/01/why-software-stocks-are-getting-pummelled

The threat investors fear is that Claude and others will destroy the SaaS value proposition because:

Limited barriers to entry: your nephew can theoretically replicate Slack with a simple prompt

Obsolescence: if I can get Claude Cowork to fetch my customers and contact them, why would I even need a campaign management tool?

AI didn’t destroy those stocks’ value. It revealed that the value was never quite there to begin with.

But this is wrong. Or at least, mostly wrong. Why? Because most software’s economic moat is not just the codebase, it is its network effect and reliability: companies (even OpenAI) use Slack because it’s a complete software with tons of integrations out of the box. Replicating it could be now easier in theory. But building up such a vast Software and maintaining it is another story. It is far easier for a company to pay $10 per user not to think about it.

AI didn’t destroy those stocks’ value. It revealed that the value was never quite there to begin with.

We’ve built RAST to do exactly one thing: compare a company’s market price to what its current and future cash flows actually justify. The overvaluation of most SaaS has been quite obvious to RAST users for a while. These stocks aren’t collapsing because AI is eating them. They’re collapsing because their price is simply correcting to a fair value.

Let’s look at three concrete examples illustrating this.

Netflix, Atlassian and Duolingo: the price simply didn’t add up

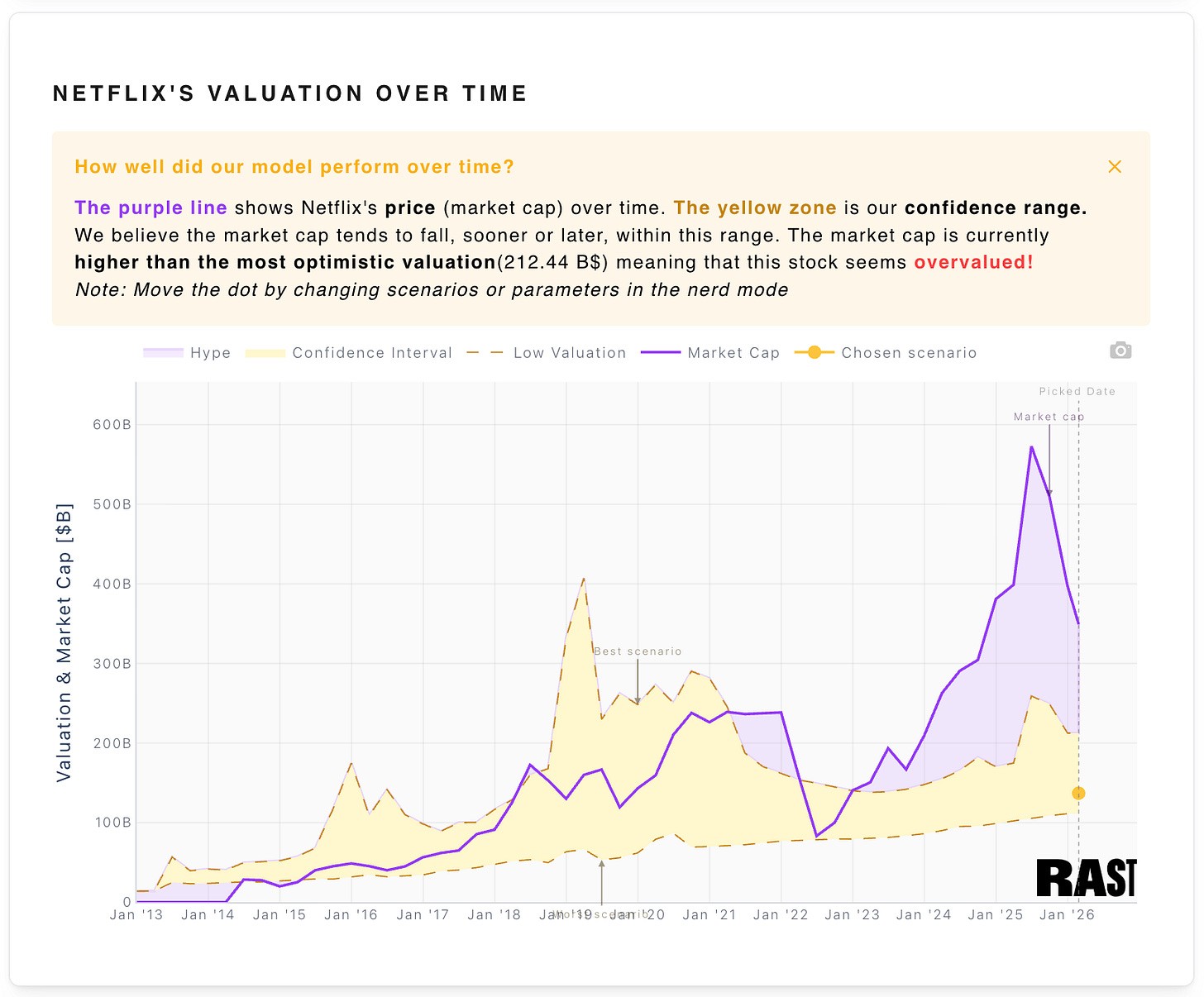

We’ve already talked lately about Netflix. The headline numbers look fine: revenues growing, margins expanding, ad-tier gaining traction. But when you look at what drives Netflix’s value (its paid memberships) the trajectory tells a different story.

The end of Netflix’s revenue growth is predictable and so is its value. Spoiler alert: it’s significantly lower than where it has traded until now.

Netflix’s market price soared well beyond RAST’s estimated intrinsic value until now (2026). The current reset is not about AI disrupting Netflix: it is about coming back to reality.

In our absolute best-case scenario, Netflix is worth somewhere around $250B, even though it was priced at nearly the double that ($573B) in May ‘25.

Nobody’s going to build Netflix’s competitor with a prompt any time soon. The valuation gap simply needed a trigger.

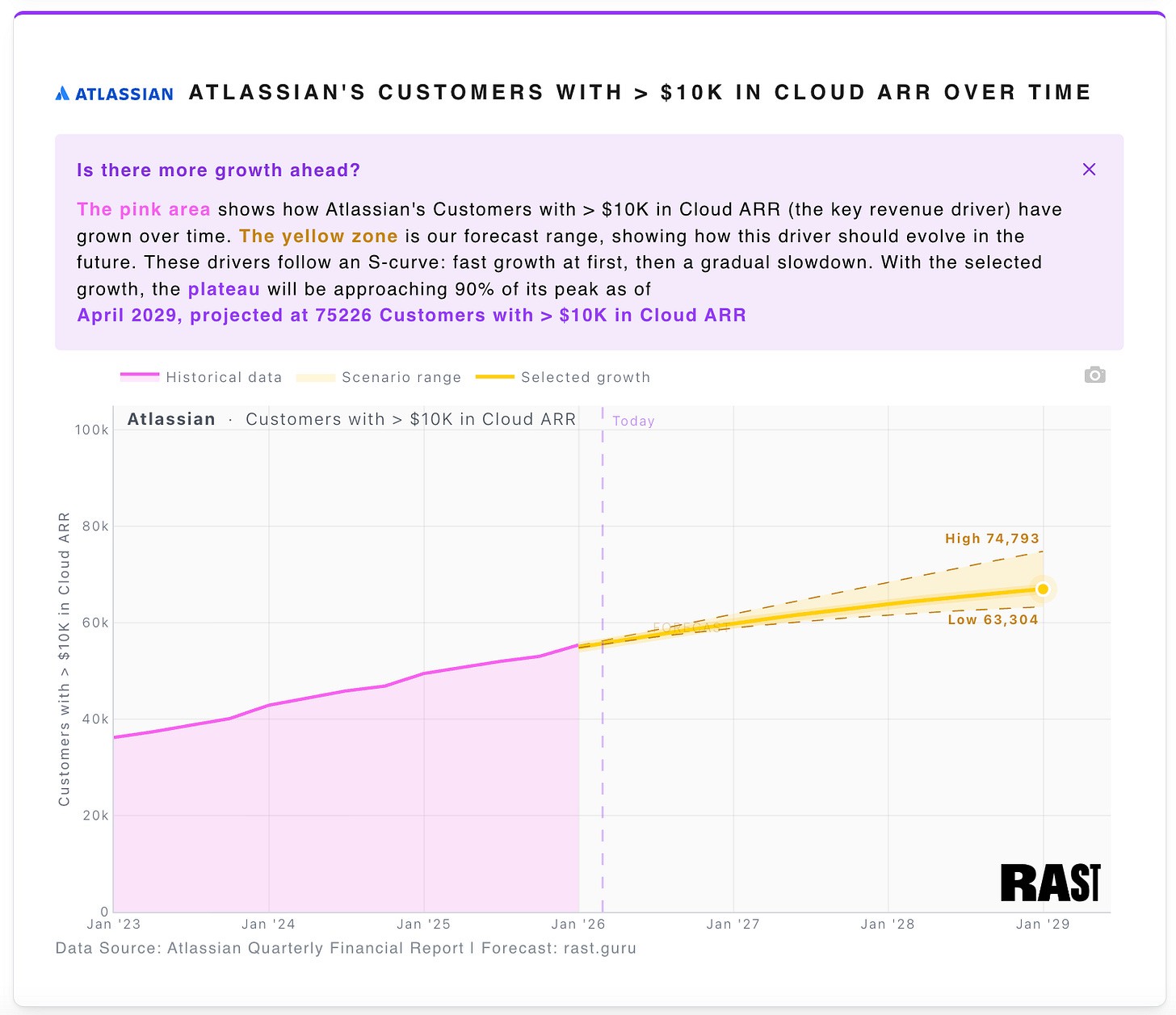

The story is similar for Atlassian, the company building Jira, the software management tool.

It just beat our best case scenario in terms of Customers >$10K in Cloud ARR. And yet, the stock hasn’t stopped plunging. Because of AI? Maybe. Because it was overvalued in the first place? Certainly.

Atlassian’s customers are growing steadily and so is their revenue per customer (ARPU). AI may be disrupting Atlassian’s business, but if it is, it is seriously taking its time.

Atlassian’s case is particularly interesting, because it’s not just a SaaS. It’s a SaaS coordinating developers’ work. With the latest LLMs, we’re starting to imagine a world where fewer developers could be needed. But given Atlassian’s sustained growth, this hasn’t started yet and will not start any time soon.

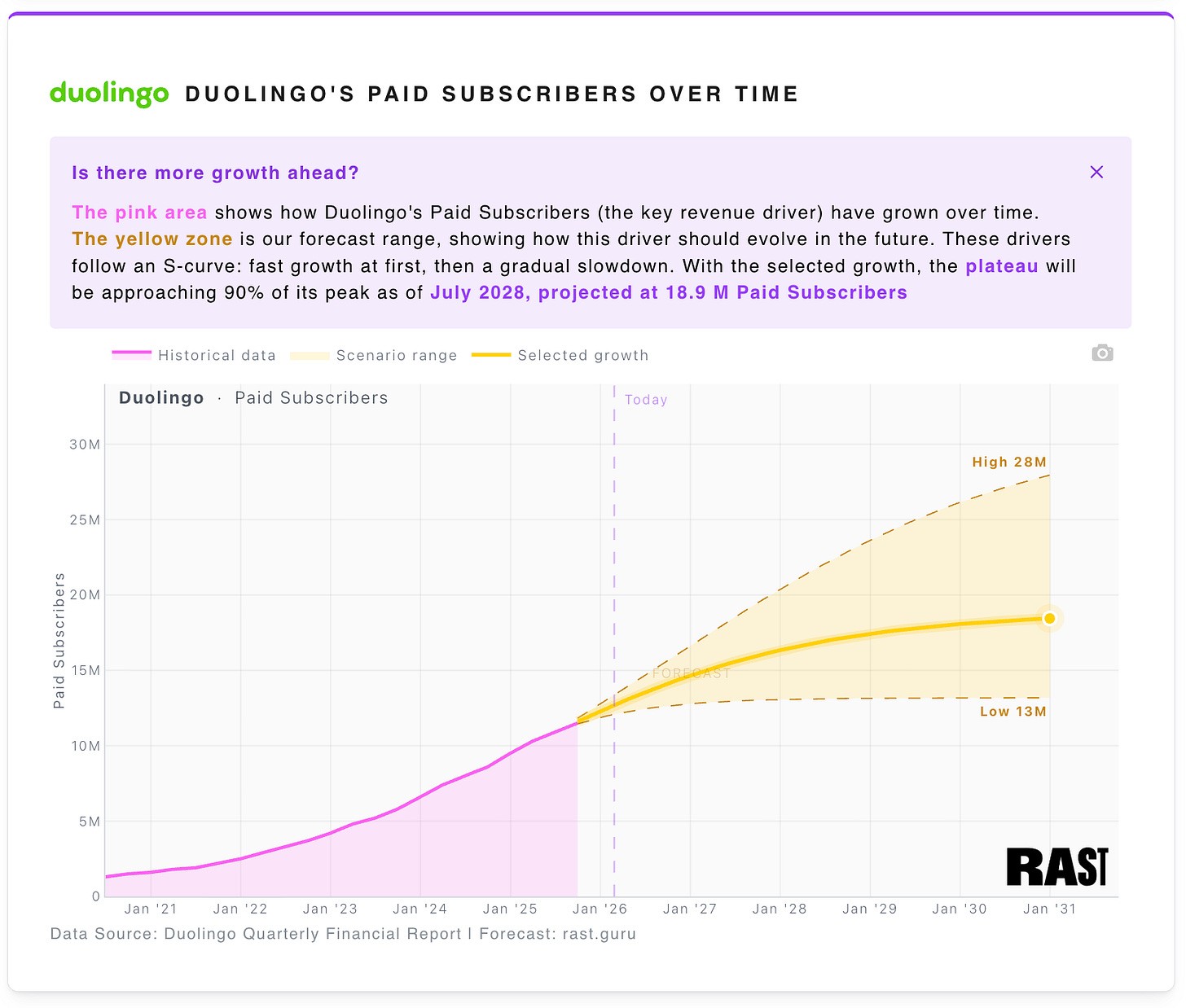

Finally the Duolingo example.

The AI disruption thesis would be: why would you pay for a gamified app to learn French when you can converse with a near-perfect AI language tutor for $20 a month (or even for free)?

That’s completely missing the point though. Duolingo isn’t really an educational tool. It is rather an addictive game. And people are not playing with ChatGPT (yet at least), they’re playing with AI wrappers.

Duolingo’s not going to be disrupted by AI. On the contrary, it’s going to boost its margins by supporting more languages with fewer employees.

The reason for the downfall is again the same: an initial overvaluation not a potential disruption by AI.

With this type of growth in terms of Paid Subscribers, it will take another couple of iterations before AI disrupts Duolingo’s business.

AI has already started to disrupt companies. But only specific

Netflix, Atlassian and Duolingo all have something in common: their price plunged even though they’ve announced record quarters. All of this because investors fear AI could be a threat to them.

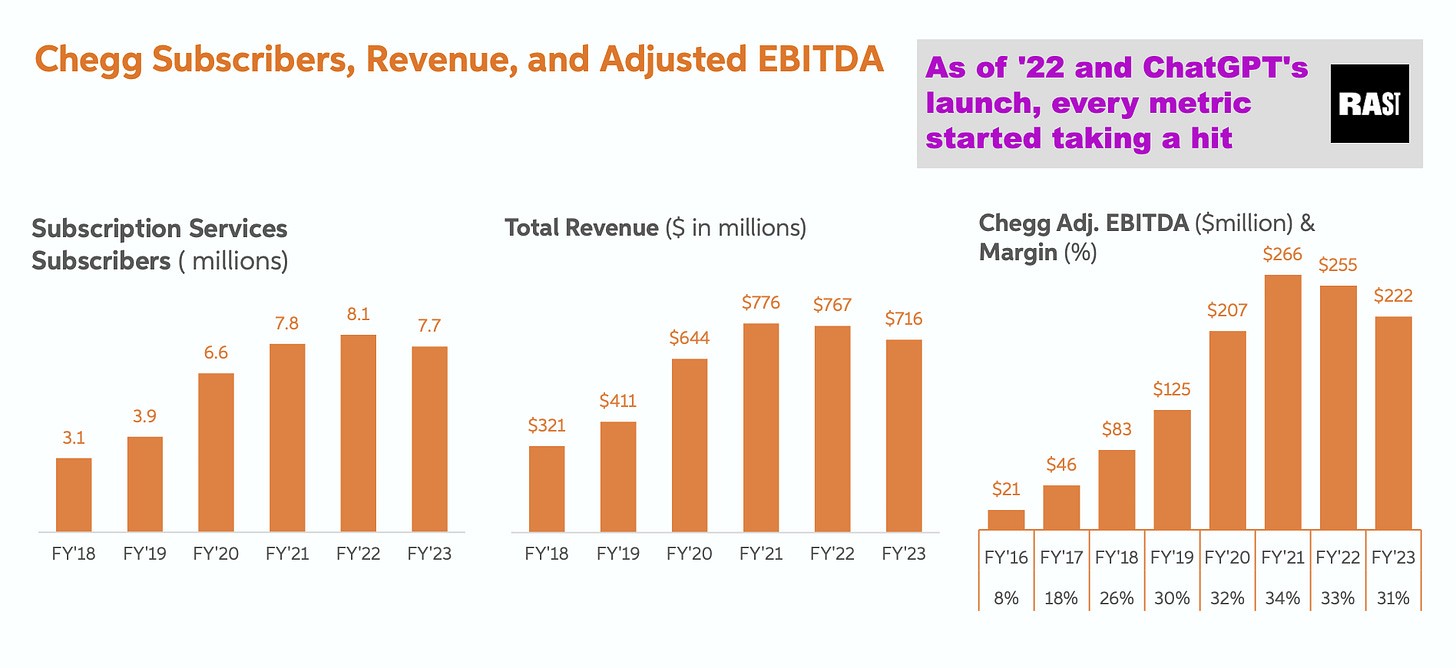

But if AI were indeed a threat, its effect would have already been visible, it would show in the data. Ask people at Chegg. The once successful ‘homework support app’ has been immediately hit by ChatGPT: why would you pay for a tutor when you can ask directly an AI to correct (or even write) your essay?

In Chegg's case, AI's effect has immediately impacted the fundamentals.

What to Watch From Here

If AI were a serious mid-term threat to Netflix, Atlassian or Duolingo1 and other SaaS, the effects would already be visible in the data. They aren’t. Their fundamentals remain solid with growing user bases and increasing revenue per user (ARPU).

The recent panic has primarily corrected mostly tech companies that were simply overvalued in the first place. The correction, however, is creating some interesting opportunities for investors. Because even though some SaaS may be disrupted in the short/mid-term by AI, the majority of established platforms will likely continue to prosper.

Atlassian and its peers may eventually face serious disruption from AI, but that transition will take time. Until then, the fundamentals should be your guide.

None of this should be considered as investment advice. We have no ties with Netflix, Atlassian or Duolingo. They are just good examples illustrating our point :).